Money Moves: A CRUT Strategy for Diversifying Concentrated Stock

Imagine selling a highly appreciated asset without triggering immediate capital gains tax, while also creating a long-term income stream and supporting charitable causes you care about. For many high-net-worth clients, this is exactly what a Charitable Remainder Unitrust, or CRUT, is designed to do.

For founders, executives, and investors with large unrealized gains, a CRUT strategy offers a way to diversify, generate income, and give strategically.

In this post, we explore how a CRUT strategy works, who it’s designed for, and how investors can use it to diversify appreciated assets while generating income and supporting charitable giving.

🧩 The Strategy: Charitable Remainder Unitrusts (CRUTs)

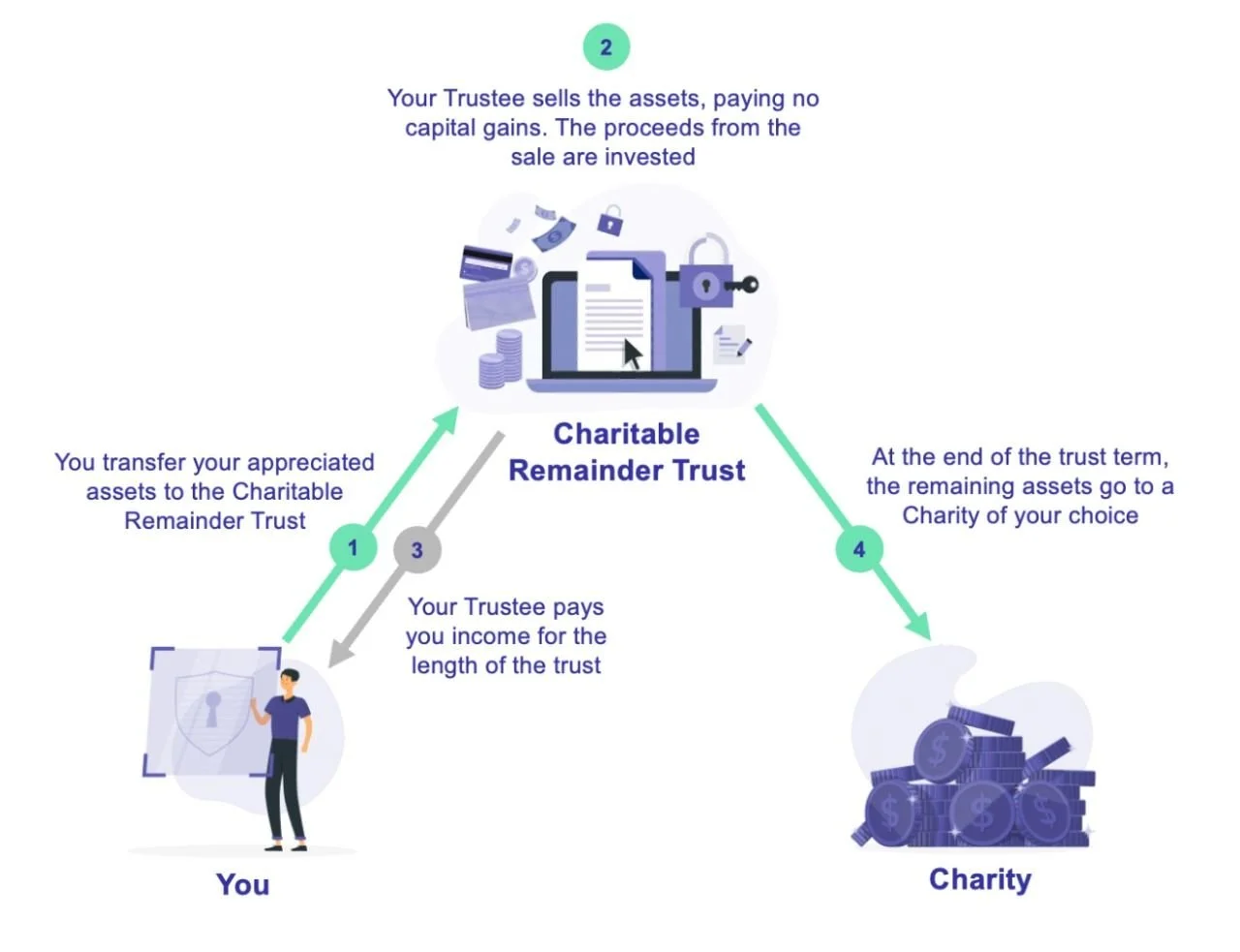

A CRUT is an irrevocable trust that converts appreciated assets into income while reserving the remainder for charity.

You contribute appreciated assets to the trust. The trust sells them without immediate recognition of capital gains and reinvests the proceeds. Each year, you receive a payout based on a fixed percentage of the trust’s value.

At the end of the trust term or upon the trustor's death, the remaining assets are distributed to qualified charitable organizations.

4 Key Features of a CRUT

Annual income based on a percentage of trust value

Capital gains tax deferred inside the trust

Partial charitable income tax deduction at funding

Charitable remainder paid at trust termination, and can be kept under some control by electing to use a Donor-Advised Fund as the chosen charity

In essence, a CRUT balances income, tax deferral, and philanthropy.

👤 Eligibility: Who Should Consider a CRUT

CRUTs work best for individuals with both financial and charitable objectives.

The ideal candidate holds highly appreciated assets and is looking for ways to diversify their holdings without triggering immediate tax consequences. They prefer to generate ongoing income rather than receive a one-time lump sum and have an established intent to support charitable causes as part of their financial and legacy planning.

4 Key Requirements

The trust must be irrevocable. (You can’t get the shares/funds back once the trust is funded)

Payout percentage must meet IRS guidelines

Remainder interest must satisfy charitable minimums

Trust administration must follow strict compliance rules

Timing Considerations

CRUTs are typically established prior to a liquidity event, particularly when the underlying asset is highly appreciated. Planning in advance allows donors to maximize both tax efficiency and income potential. If the contributed assets are subject to trading windows or other restrictions, those timing requirements must also be followed.

Money Moves in Real Life: Client Diversifies a Concentrated Nvidia Position with a CRUT

Client Background

An early Nvidia employee held a significant portion of their wealth in a single Nvidia stock position. Over time, the shares had appreciated substantially, leaving the client with over 80% of their net worth tied to one company.

While confident in the company’s long-term prospects, the client recognized the risk of such heavy concentration. However, selling the shares outright would have triggered a large capital gains tax bill.

The client also had limited immediate income needs and was already charitably inclined.

Planning Process

We worked with the client to develop a comprehensive financial plan and evaluate several diversification strategies.

After modeling different scenarios, we implemented a CRUT funded with a portion of the concentrated stock position.

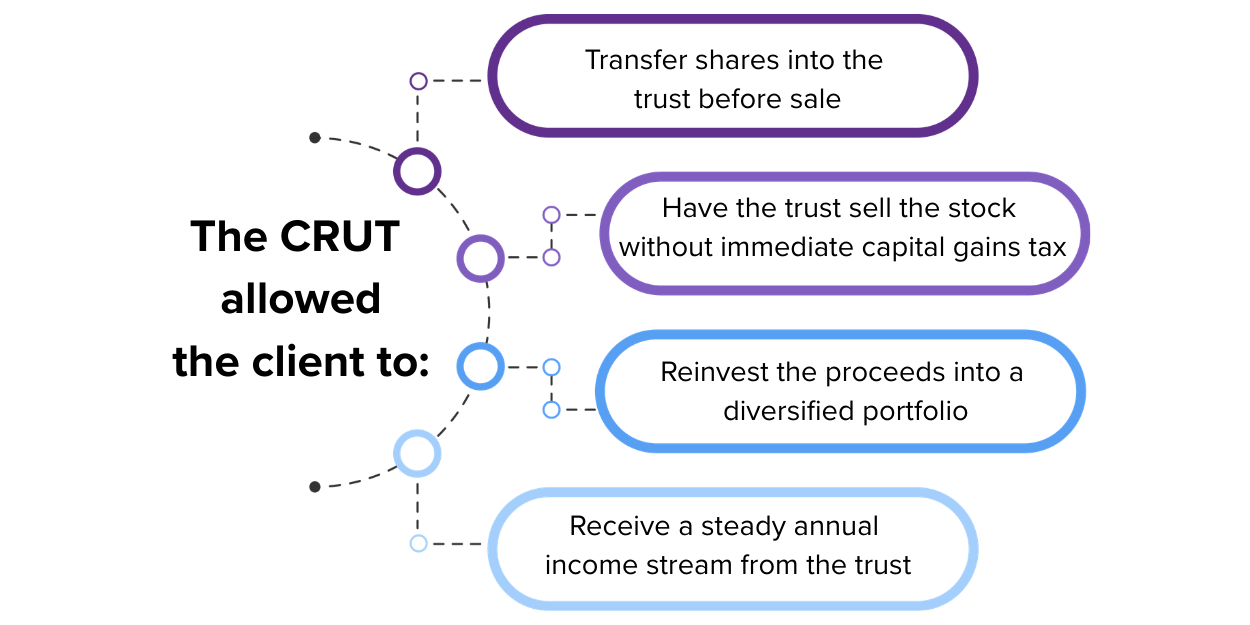

The CRUT allowed the client to:

Transfer shares into the trust before sale

Have the trust sell the stock without immediate capital gains tax

Reinvest the proceeds into a diversified portfolio

Receive a steady annual income stream from the trust

Because the trust included a charitable remainder, the client also received a significant charitable income tax deduction, which helped offset other taxable income that year.

Outcome

The strategy delivered several meaningful benefits, both financial and personal. It reduced the client’s concentration risk in a single stock, bringing greater balance and peace of mind to their portfolio. At the same time, it created a reliable lifetime income stream tied to the value of the trust, providing long-term financial stability.

The structure also generated a meaningful charitable tax deduction while enabling the client to support causes that were deeply important to them.

Most importantly, it allowed the client to diversify strategically without the immediate tax friction of selling the shares outright, turning a concentrated position into a source of stability, income, and lasting charitable impact.

5️⃣ Key Takeaways

CRUTs defer capital gains rather than eliminating them

Income is flexible and tied to trust performance

Charitable giving is a required component

Diversification can occur inside the trust

Irrevocability requires thoughtful planning

✏️ Advanced Tip

For charitably inclined investors, CRUTs can also complement other strategies, including:

Qualified Small Business Stock (QSBS) planning

Estate planning strategies

Donor-advised funds or private foundations

When integrated into a broader plan, they can play a powerful role in tax management, income planning, and legacy giving.

Conclusion

CRUTs are not just tax strategies. They are planning strategies that align income, diversification, and impact. For the right client, they can turn a concentrated asset into a purpose-driven solution for reducing highly appreciated and/or concentrated positions.

Wondering how a CRUT strategy could fit into your equity or liquidity planning? Schedule a consultation to explore whether this strategy aligns with your goals.

DISCLOSURES

DiversiFi Capital LLC is a registered investment adviser located in CA and may only transact business or render personalized investment advice in those states and international jurisdictions where we are registered, notice filed, or where we qualify for an exemption or exclusion from registration requirements. Any communications with prospective clients residing in jurisdictions where DiversiFi Capital LLC is not registered or licensed shall be limited so as not to trigger registration or licensing requirements.

Past performance is not indicative of future returns, and investing always carries inherent risks, including the potential loss of principal capital. Any investment strategies are specific to individual clients and may not be representative of the experiences of all clients.

The Information presented in our blog posts is intended for educational purposes only. It is not intended to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Unless otherwise stated, the investments discussed in our blog posts are not guaranteed.

The content in our blog posts is designed to provide information and insights but should not be used as the sole basis for making financial decisions. The content provided in our blog post(s) is provided “as is,” and/or “as available.” Diversifi Capital LLC will to the best of its abilities maintain the content to be up to date. However, Diversifi Capital LLC does not represent or warrant that our content or our services found within are accurate, complete, reliable, current, or error-free.

We strongly encourage readers to conduct their own research, seek advice from qualified financial professionals, and consider their unique financial circumstances before making any investment or financial decisions. Your individual situation may vary, and it's essential to make informed choices that align with your specific goals and needs.

Tax information given is provided as a general strategy and not intended as tax advice. You should consult your tax professional for clarification and any additional questions prior to implementation. Under Circular 230, the advice contained in this communication was not intended or written by the practitioner to be used, and it cannot be used by the taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service.

Case studies presented are based on actual clients, however, some of the information may have been changed or altered. These studies are provided for educational purposes only. Similar, or even positive results, cannot be guaranteed. Each client has their own unique set of circumstances so products and strategies may not by suitable for all people. Please consult with a qualified professional before implementing any strategy discussed herein.