Case Study: Building Our Starter Client’s Financial Foundation

Disclosure:

Case studies presented are based on actual clients, however, some of the information may have been changed or altered. These studies are provided for educational purposes only. Similar or even positive results cannot be guaranteed. Each client has their own unique set of circumstances, so products and strategies may not be suitable for all people. Please consult with a qualified professional before implementing any strategy discussed herein.

Meet Stacy and Jim, a young Starter-level family living in New York with two kids, primarily supported by one income from working at Opus. They had built up meaningful savings, had no debt, and were generally managing their day-to-day finances well.

However, beyond that, their finances lacked structure. Most of their money was cash; they weren’t investing, didn’t have retirement accounts set up, and weren’t sure if they were being tax-efficient.

They came to their advisor, Thomas, with a simple but important question: “We have money… what should we be doing with it?”

In this interview, Thomas shares his perspective on what it was like to work with this Starter-level couple to help them build their financial foundation and move from uncertainty about their finances to ongoing empowered decisions about their lives and futures.

The Challenge

“What challenges or opportunities were your clients facing around organizing their finances/budgeting, and what led them to seek your help?

How do you think they were feeling at the time?”

Jim and Stacy were not in a bad financial place to start. They were just new to finance and seeking support.

“Jim and Stacy weren’t in a bad financial position, but they lacked clarity and direction about how to organize and manage their finances.

They had savings, no debt, and a stable income, but:

All of their money was sitting in cash

They didn’t have an investment strategy

They didn’t have a clear understanding of their net income and were overwithholding on their taxes.

They didn’t have a clear system for managing cash flow

They weren’t sure if they were making the most of their money

Their spending also felt hard to interpret. They had recently moved, which led to large one-time expenses, and they regularly had variable costs like travel and kids’ activities. This made it difficult to understand what their “normal” spending actually looked like.

Stacy described having “no idea where to start” when it came to investing and financial planning, and low confidence in making decisions.

Emotionally, they both felt unsure whether they were doing things correctly, slightly anxious about their lack of progress, and aware they should be doing more, without a clear sense of what that actually meant.

At this juncture, they weren’t looking for complexity or aggressive strategies; instead, they were seeking guidance on structuring their accounts, investing appropriately, and making confident, informed decisions with their money.”

Thomas’s Approach

“How did you help your client organize and manage their finances (i.e., reason for soliciting your help)?

What was your approach? What behavioral barriers or biases, if any, did you identify and address?”

The primary focus became building their foundation first, and then working from there to help our clients make new, more empowering decisions.

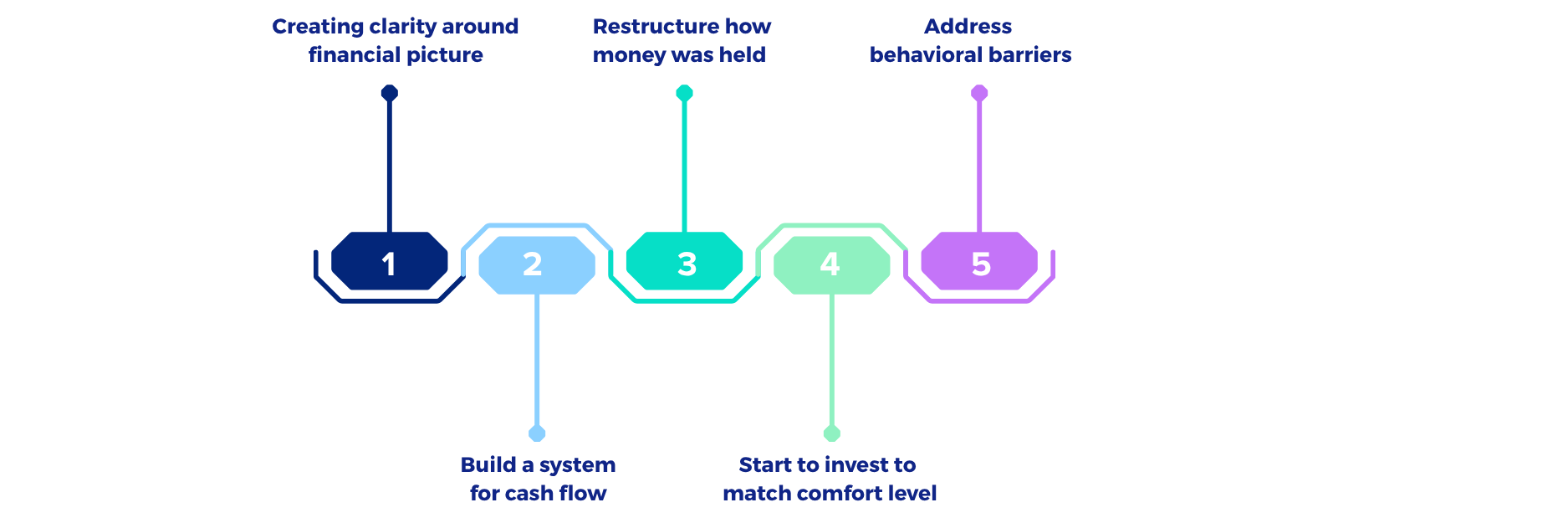

“My approach focused on building a foundation before introducing complexity.

1. Creating clarity around their financial picture

I started by organizing their finances into a clear structure, which included:

Understanding true take-home income

Separating regular or recurring monthly spending from one-off expenses

Mapping where their money currently sits

A key shift was helping them distinguish between irregular spending (like furnishing a home) and their ongoing baseline. This made their finances feel less overwhelming and more predictable.

2. Building a simple, sustainable system for cash flow

Rather than strict budgeting, I worked with them to focus on awareness and consistency.

I guided them through:

A simple monthly review of spending

A clearer breakdown of categories

A shared process for discussing money as a couple

This reduced ambiguity and helped them make decisions more intentionally.

3. Restructuring how their money was held

A major issue was that all of their money was sitting in easily accessible cash, well beyond what they needed for an emergency fund and near-term expenses. Using a framework like 50/30/20, this meant a disproportionate share of their resources was sitting idle instead of being allocated toward longer-term goals.

I helped them:

Open a brokerage account

Move excess cash out of savings

Start using low-risk, liquid investments

This allowed their money to begin working while also creating a small layer of discipline around spending.

I also helped Jim adjust his withholding to avoid large tax refunds. Moving forward, withholding would reflect the actual end-of-year tax liability, thereby ensuring we made more money available on a monthly basis.

4. Starting to invest in a way that matched their comfort level

Stacy was very risk-averse, which had led to inaction. Instead of pushing her toward complex strategies, I focused on helping her build confidence first, starting with education, walking through transactions step-by-step, and encouraging her to begin with small, manageable actions.

5. Address behavioral barriers

I also addressed several key behavioral barriers that were holding them back. These included risk aversion that led to avoiding investing, too much cash accessibility that made overspending easier, and limited visibility into their finances, which created uncertainty and hesitation.

Underneath it all was a lingering “we should already know this” mindset that was quietly reducing their confidence.

The goal was to replace these patterns with a stronger foundation built on:

Clear understanding

Intentional structure

Small, repeatable actions they could consistently follow.”

The Outcome

“What outcome was ultimately achieved for Stacy and Jim through this support? How did they feel after?”

Teaching our clients foundational knowledge about their finances gave them the confidence to take control of how they build their financial future and reach goals that are meaningful to them.

The outcome was a shift from uncertainty to understanding their finances and moving forward with a new level of confidence.

Stacy and Jim:

Gained a clear understanding of their cash flow

Built a structured system for managing finances

Opened and began using an investment account

Set up monthly automated investments into a diversified, low-cost portfolio

Moved their emergency fund out of savings into a higher-yield money market fund

Even early actions, like making their first investment, created a meaningful sense of progress. At one point, they described the experience as “opening up a whole new world” in terms of what they could do with their money.

Emotionally, the shift was just as important. They moved from confusion to understanding, hesitation to action, and from being passive with their finances to being fully engaged.

They weren’t trying to optimize everything overnight, but they finally felt like they were on track.”

Better Money Habits Over Time Leading to Better Future Outcomes

How has this experience changed your client’s behavior or mindset around their finances moving forward, and what long-term impact do you expect it to have?

“The biggest change was in how they approach their finances day to day.

Before our work together, their approach to finances was largely reactive. Spending decisions were loosely tracked, and saving and investing lacked clear intention. This often left them feeling unsure if they were doing things correctly, slightly anxious about their lack of progress, and aware they should be doing more without a clear sense of what that meant.

Now, they operate with a clearer system for reviewing and managing money. They are more deliberate about how they allocate cash, actively engage with investing rather than avoiding it, and rely on a shared framework when making financial decisions. As a result, they feel more in control, more confident in their choices, and less uncertain about what actions to take.

They have also begun thinking more carefully about tradeoffs, aligning their spending with what matters most to them, and building habits like regular financial check-ins.

Over the long term, this shift is likely to lead to more consistent saving and investing, better use of future income and equity, and greater financial confidence and stability. Most importantly, they have moved from asking “What should we do?” to feeling empowered to answer that question themselves.”

Ready to get started on your financial wellness journey?

DiversiFi Capital Inc. is a registered investment adviser located in CA and may only transact business or render personalized investment advice in those states and international jurisdictions where we are registered, notice filed, or where we qualify for an exemption or exclusion from registration requirements. Any communications with prospective clients residing in jurisdictions where DiversiFi Capital Inc. is not registered or licensed shall be limited so as not to trigger registration or licensing requirements.

Past performance is not indicative of future returns, and investing always carries inherent risks, including the potential loss of principal capital. Any investment strategies are specific to individual clients and may not be representative of the experiences of all clients.

Case studies presented are based on actual clients, however, some of the information may have been changed or altered. These studies are provided for educational purposes only. Similar or even positive results cannot be guaranteed. Each client has their own unique set of circumstances, so products and strategies may not be suitable for all people. Please consult with a qualified professional before implementing any strategy discussed herein.

DiversiFi Capital is not affiliated with the company mentioned herein.