Psychology of Investing: How Emotions Impact Equity Decisions

Equity decisions are not purely financial. They're often emotional, and the emotional dimension is frequently the part that actually drives what people do.

For many individuals who work in tech, their company represents years of work, belief in the mission, and pride in building something meaningful. Because of that, selling shares can sometimes feel uncomfortable even when diversification is financially sensible.

Understanding the emotional influences at play doesn't make them go away. But it can help you recognize when they're driving your decisions, and create structures that keep your financial plan on track regardless of how you are feeling.

In this post, we dive into the psychology of investing and how emotions influence decisions around equity compensation, why selling company stock can feel harder than it should, and how to build structures that keep your financial plan on track.

Why Selling Can Feel Harder Than It Should

The math of diversification is usually straightforward. An employee with 50% of their net worth in a single stock faces more risk than one with 15%. A diversified portfolio has better risk-adjusted returns over time. The tax strategies for reducing concentration are well understood.

And yet, the decision to sell is often the hardest financial decision tech employees face. There are a few reasons for that, and none of them are about analysis.

Loss Aversion and Anchoring

When the stock rises, holding feels exciting. When it falls, selling can feel like locking in a loss. That second reaction is loss aversion at work: we tend to feel losses more acutely than equivalent gains, which makes selling below a reference point genuinely painful, even when that reference point has no bearing on what the stock will do next.

Anchoring compounds this. Employees often fixate on a reference price, the price at the time of their grant, a recent high, or the price they "should have sold at." But that reference point is irrelevant to the forward-looking decision. Both the loss aversion and the anchor are distractions from the questions that actually matter: Is this a good investment moving forward? What is a reasonable amount of my net worth to put into this bet?

If you find yourself thinking "I'll sell when it gets back to $X," that's a signal that anchoring is driving the decision, not analysis.

Familiarity Bias

Because employees understand their company deeply, the product, the roadmap, and the competitive landscape, your company's stock can feel safer than other investments. You know things about this company that you don't know about the S&P 500, and that knowledge creates a sense of comfort.

But familiarity isn't the same as safety. Having both your income and your investments tied to the same company increases your financial risk, even if your understanding of the business is excellent. The risk isn't that you're wrong about the company; it's that a single outcome, whether it's a market correction, a regulatory event, a change in the competitive landscape, or a shift in sentiment, affects everything at once.

The Inertia Problem

One of the most powerful forces in equity compensation isn't conviction or analysis; it's doing nothing. Holding is the default. It requires no action, no paperwork, no confrontation with the decision. Selling, by contrast, feels like an active choice with consequences. For many people, that inertia is driven by emotion: a fear of missing out on future gains, or a fear of making the wrong move and regretting it. Behavioral scientists call this the status quo bias, and it's well documented.

This asymmetry means that many employees end up holding not because they've decided to hold, but because they haven't decided not to hold. Over time, that inertia can build a concentrated position that no rational investor would construct from scratch.

If you received the value of your vested shares as cash today, would you invest it all in your company's stock? If the answer is no, inertia or loss aversion may be the reason you're still holding.

Identity and Loyalty

For employees at mission-driven companies, selling stock can feel like a vote of no confidence. There's a sense, sometimes explicit in company culture, sometimes unspoken, that real believers hold.

This conflation of investment decisions with company loyalty is a costly emotional pattern in equity compensation, but it's not uniquely so. Your belief in the company's mission and your decision about portfolio allocation are genuinely separate questions. You can be deeply committed to your company's success and still conclude that holding 40% of your net worth in a single stock carries more risk than your financial plan warrants.

Diversification isn't a judgment about the company's future. It's a decision about how much risk you want to take on with your personal finances.

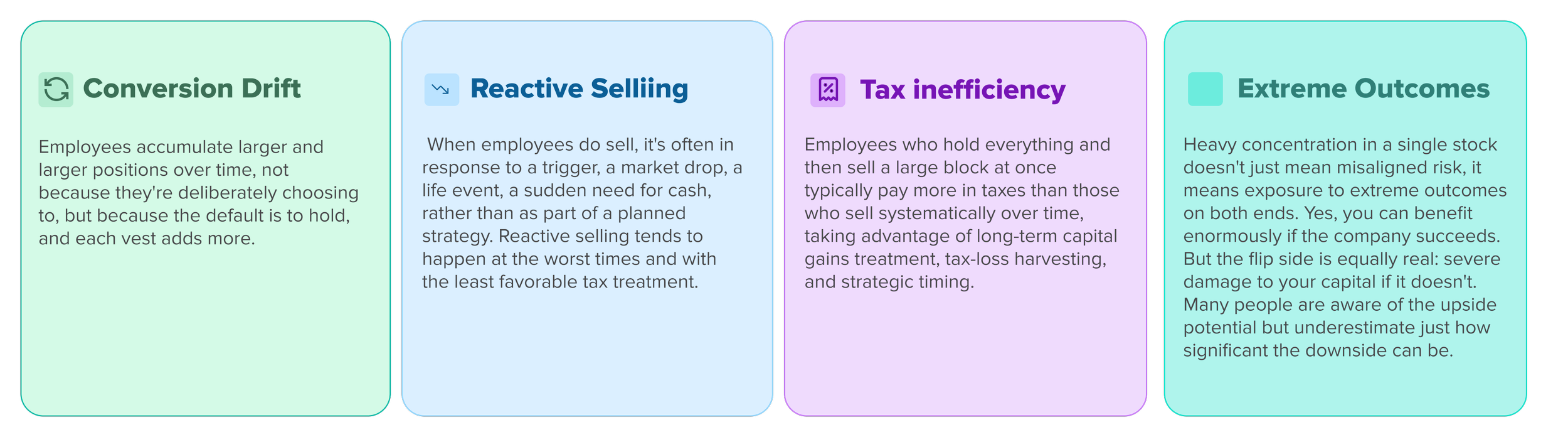

The Cost of Emotional Investing

The emotional patterns described above tend to produce a consistent set of outcomes when left unaddressed:

Structures That Help

Understanding the psychology of investing and managing the emotional side of equity decisions isn't purely about willpower. It starts with awareness: understanding which psychological tendencies are at play for you around equity compensation, and then putting structures in place to navigate them.

A systematic selling strategy. Decide in advance what percentage of each vest you'll sell. Make the decision once, during a calm period, and execute it consistently. This removes the emotional weight from each individual vesting event.

A target concentration ceiling. Define the maximum percentage of your net worth you're comfortable holding in a single stock. When you cross that threshold, sell to bring it back in line. The threshold does the deciding for you.

A 10b5-1 plan. For employees who find the act of selling particularly difficult, a pre-scheduled trading plan automates the execution entirely. The trades happen regardless of what the stock did last week or how you feel about the company today.

Connecting sales to goals. When you sell to fund a down payment, a child's education, or your long-term financial independence, the transaction stops feeling like a loss and starts becoming a source of progress. Tying equity to specific goals is one of the most effective ways to dissolve the emotional friction of selling.

Tax-aware strategies for when selling feels too costly. If the tax consequences of selling are part of what's holding you back, there are structured solutions worth exploring. Tax exchange funds and long-short funds, for example, can help reduce concentration without requiring a direct sale, which can ease the decision significantly.

A Different Way to Think About It

The employees who navigate equity compensation most effectively tend to share a common trait: they're able to separate their emotions from their decisions about portfolio allocation. That's easier said than done, because company stock doesn't feel like just another investment. But that's exactly what it is. Just because you received it as compensation doesn't change what it is: an investment that should be evaluated on its own merits, the same way you'd evaluate anything else in your portfolio.

These are genuinely different questions. "Do I think this company will succeed?" is a question about the business. "Should 40% of my net worth be in this stock?" is a question about risk management. You can answer the first question with conviction and the second with caution, and that's often the wisest combination.

The goal isn't to eliminate emotion from equity decisions. It's to recognize when emotion is driving the decision, and to have structures in place that keep your financial plan intact regardless. If you recognize these patterns in your own decision-making, the first step is simply to name them. The second is to build a plan that doesn't depend on overcoming them in the moment.

Getting Started

That's one of the things we help clients with. Not just the analysis of what to hold and what to sell, but the behavioral framework that makes execution possible.

If making decisions about your equity feels unusually difficult, or you feel that fear, excitement, uncertainty, or other strong emotions are influencing your thinking, a structured decision-making process can help bring clarity.

Schedule a free consultation with us today.

DISCLOSURES

DiversiFi Capital LLC is a registered investment adviser located in CA and may only transact business or render personalized investment advice in those states and international jurisdictions where we are registered, notice filed, or where we qualify for an exemption or exclusion from registration requirements. Any communications with prospective clients residing in jurisdictions where DiversiFi Capital LLC is not registered or licensed shall be limited so as not to trigger registration or licensing requirements.

Past performance is not indicative of future returns, and investing always carries inherent risks, including the potential loss of principal capital. Any investment strategies are specific to individual clients and may not be representative of the experiences of all clients.

The Information presented in our blog posts is intended for educational purposes only. It is not intended to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Unless otherwise stated, the investments discussed in our blog posts are not guaranteed.

The content in our blog posts is designed to provide information and insights but should not be used as the sole basis for making financial decisions. The content provided in our blog post(s) is provided “as is,” and/or “as available.” Diversifi Capital LLC will to the best of its abilities maintain the content to be up to date. However, Diversifi Capital LLC does not represent or warrant that our content or our services found within are accurate, complete, reliable, current, or error-free.

We strongly encourage readers to conduct their own research, seek advice from qualified financial professionals, and consider their unique financial circumstances before making any investment or financial decisions. Your individual situation may vary, and it's essential to make informed choices that align with your specific goals and needs.

Tax information given is provided as a general strategy and not intended as tax advice. You should consult your tax professional for clarification and any additional questions prior to implementation.