Social Security 101

Social Security is one of the cornerstones of retirement income in the United States, yet few people fully understand how it works or how much they might receive. While it was designed to provide a safety net, Social Security benefits can also be a key piece of a broader financial plan when used strategically.

Even if retirement feels far away, the decisions you make in your 30s and 40s can directly influence what your Social Security record looks like down the road. For professionals building wealth through equity compensation, bonuses, or career transitions, understanding how Social Security fits into your larger plan can help you make smarter tax and income decisions.

In this post, we’ll cover what Social Security is, how benefits are calculated, when you can start claiming, and strategies to help you make the most of your benefits.

Why Paying Attention to It Now Matters

You’re already contributing to Social Security with every paycheck, so it’s worth understanding how this system affects your financial picture now, not just in retirement.

Here’s why it’s worth paying attention earlier than you might think:

Your lifetime earnings record starts now, and the Social Security Administration uses your 35 highest earning years to calculate benefits.

Your current high-income years or stock-based compensation events may replace lower-earning years, increasing your benefit base.

Knowing how Social Security interacts with your other income streams can help you plan for taxes, savings, and financial independence.

If you take a career break, switch industries, or start your own venture, knowing how benefits accrue can help you maintain your credits and avoid surprises later.

Understanding how the system works today helps you build confidence and flexibility for the long term. It’s less about preparing for retirement and more about building a foundation for financial independence.

What Is Social Security and How Does It Work?

Social Security is a federal program that provides monthly retirement, disability, and survivor benefits to eligible individuals and their families. It’s funded through payroll taxes that you and your employer pay throughout your working years.

Here’s how it works:

You earn “credits” for work. In 2025, you earn one credit for every $1,730 in wages, up to four credits per year. Most people need 40 credits (about 10 years of work) to qualify for benefits.

Your benefit is based on your lifetime earnings. The Social Security Administration (SSA) uses your 35 highest earning years, adjusted for inflation, to calculate your benefit amount.

You can claim benefits as early as age 62. But the longer you wait (up to age 70), the higher your monthly benefit will be.

While Social Security alone is rarely enough to replace your full income, it’s an important foundation that can complement savings, investments, and employer benefits.

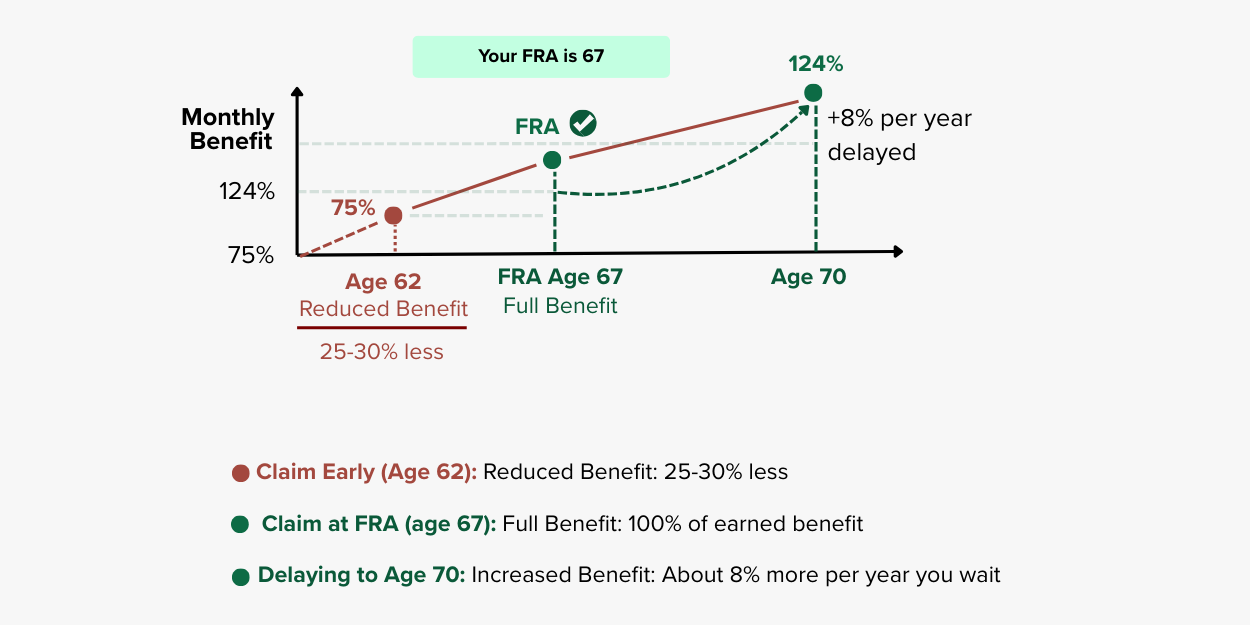

When Should You Claim Social Security?

Choosing when to start receiving benefits is one of the most important retirement decisions you’ll make. Your Full Retirement Age (FRA) determines when you’re eligible to receive your full benefit amount.

For anyone born in 1960 or later, the FRA is 67. That means if you claim before age 67, your monthly benefit will be permanently reduced, and if you wait past 67 (up to age 70), your monthly benefit will increase by about 8% for each year you delay.

Here’s how timing affects your monthly payment:

Claiming early (age 62): You’ll receive reduced benefits for life (about 25–30% less).

Claiming at FRA (age 67): You’ll receive 100% of your earned benefit.

Delaying past FRA (up to age 70): Your benefits increase by about 8% per year you wait.

For higher-income earners and those with substantial retirement savings, delaying benefits can make sense as part of a long-term tax and income strategy.

How Benefits Are Taxed

Many people are surprised to learn that Social Security benefits can be taxable. The percentage you owe depends on your combined income, which includes:

Adjusted gross income (AGI)

Nontaxable interest (such as municipal bond income)

Half of your Social Security benefits

Depending on your total income, up to 85% of your benefits could be subject to federal income tax.

For professionals with equity compensation or significant investment income, timing can make a major difference. Coordinating when to exercise options, sell stock, or begin taking distributions from retirement accounts can help reduce your tax burden in the years you receive Social Security.

Understanding how Social Security fits into your overall tax picture can be complex, especially if you have multiple income sources or equity compensation. A DiversiFi advisor can help you evaluate how your current earnings and future benefits work together, so you can plan confidently for the years ahead. Schedule a consultation with us today.

Spousal and Survivor Benefits

Social Security also provides benefits to your spouse or eligible dependents.

Spousal benefits: A spouse can claim up to 50% of your benefit if it’s higher than their own.

Survivor benefits: If you pass away, your spouse and eligible children may receive benefits based on your earnings record.

Divorced spouses: If you were married for at least 10 years and haven’t remarried, your ex-spouse may also qualify for benefits based on your record.

These benefits can make a meaningful difference in household retirement income and should be factored into your long-term planning.

Strategies to Maximize Your Social Security Benefits

While everyone’s situation is different, a few strategies can help optimize your Social Security outcome:

Delay benefits if possible. Each year you wait after your FRA adds roughly 8% to your benefit until age 70.

Coordinate with your spouse. Staggering claim dates or having the higher earner delay benefits can increase lifetime payouts.

Mind your income timing. Reducing taxable income in retirement years can minimize how much of your Social Security is taxed.

Consider your portfolio mix. Balancing Social Security with other income sources like 401(k)s, IRAs, or stock compensation can help create predictable cash flow.

Final Thoughts

Social Security is more than a retirement paycheck; it’s a foundation that you’re building right now with every paycheck you earn. For people in their 30s and 40s, the focus shouldn’t be on when to claim, but on understanding how your earnings today influence the future benefits you’ll eventually receive.

By learning how the system works early, you can plan around it rather than react to it. Integrating Social Security awareness into your long-term financial strategy, alongside equity compensation, investments, and tax planning, can help you create a more balanced and resilient path toward financial independence.

DISCLOSURES

DiversiFi Capital LLC is a registered investment adviser located in CA and may only transact business or render personalized investment advice in those states and international jurisdictions where we are registered, notice filed, or where we qualify for an exemption or exclusion from registration requirements. Any communications with prospective clients residing in jurisdictions where DiversiFi Capital LLC is not registered or licensed shall be limited so as not to trigger registration or licensing requirements.

The Information presented in our blog posts is intended for educational purposes only. It is not intended to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Unless otherwise stated, the investments discussed in our blog posts are not guaranteed.

The content in our blog posts is designed to provide information and insights but should not be used as the sole basis for making financial decisions. The content provided in our blog post(s) is provided “as is,” and/or “as available.” Diversifi Capital LLC will to the best of its abilities maintain the content to be up to date. However, Diversifi Capital LLC does not represent or warrant that our content or our services found within are accurate, complete, reliable, current, or error-free.

We strongly encourage readers to conduct their own research, seek advice from qualified financial professionals, and consider their unique financial circumstances before making any investment or financial decisions. Your individual situation may vary, and it's essential to make informed choices that align with your specific goals and needs.