Lifestyle Creep 101

Lifestyle creep is one of the most common and least discussed challenges in personal finance. It shows up quietly as income grows and small upgrades start to feel normal. The issue is not that spending on comfort or convenience is wrong. The problem is how easily higher expenses can outpace the room you actually have after taxes, long-term goals, and future needs are accounted for. This is why people often focus on better investments, when a major part of financial stability comes from managing spending as income increases.

Lifestyle creep also matters because taxes rise sharply at higher income levels, and each additional dollar earned does not translate to a dollar of new spending capacity. When spending grows at the same pace as gross income, savings rates tend to fall, and the long-term impact can be meaningful.

In this post, you will learn what lifestyle creep is, why it happens, and how to manage it in a sustainable way.

What is Lifestyle Creep?

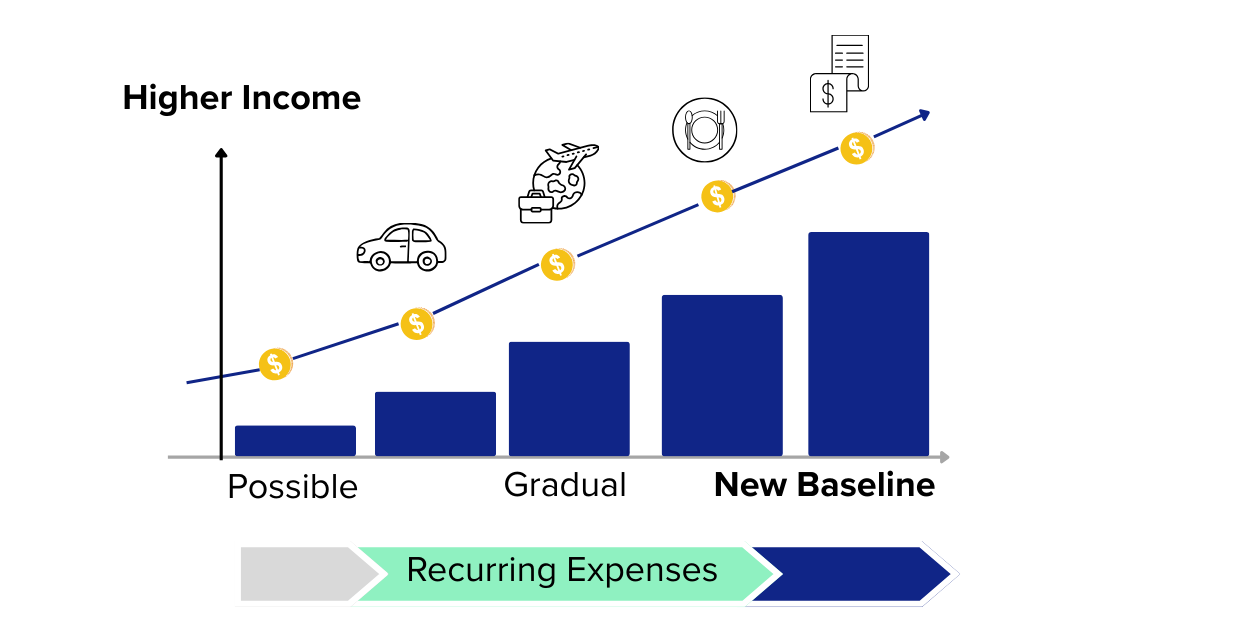

Lifestyle creep occurs when higher income leads to higher recurring expenses that eventually feel fixed. It is common as careers advance, bonuses appear more regularly, or equity compensation starts to vest. The pattern is rarely intentional. It usually comes from normal human behavior: spending slightly more because it feels possible and gradually accepting those changes as the new baseline.

This matters because after-tax income does not rise as quickly as gross income. Federal and state taxes often increase at the same time, which narrows the financial benefit of higher earnings. When recurring expenses grow at the same pace as compensation, it becomes harder to save consistently or make progress toward larger goals.

Understanding lifestyle creep is not about limiting enjoyment. It is about seeing how spending decisions today affect your future flexibility. Early habits tend to compound over time, and building strong margins while income is still growing can have a meaningful effect on long-term outcomes.

How Lifestyle Creep Starts

Shifts in Spending Patterns

Lifestyle creep often begins with small upgrades. A slightly nicer apartment, more frequent dining out, or new subscriptions can feel harmless. Over time these decisions accumulate. Many become recurring expenses that require a larger portion of your take-home income, even when the original intention was temporary or occasional.

Interaction with Taxes

Higher income often pushes you into higher tax brackets. At top marginal levels you might see rates near 37 percent federally and above 12 percent in California. This means that a raise does not translate to a proportional increase in spending power. If spending increases based on the gross number rather than the after-tax amount, savings rates can decline faster than expected.

The Role of Early Margins

Strong savings habits build on themselves. Increasing income without increasing spending at the same rate can create valuable financial margin. Established early, this margin supports future choices, including career flexibility, home purchases, and long-term investing. While investment performance often receives most of the attention, consistent savings is what gives those investments room to grow.

4 Common Mistakes Leading to Lifestyle Creep

Many people assume lifestyle creep is obvious, but it often shows up in subtle ways. Common challenges include:

Treating every raise or bonus as available spending rather than partially absorbed by taxes and goals.

Allowing recurring expenses to grow without revisiting whether they still add value.

Anchoring to peers or colleagues whose financial situations differ.

Assuming growing income will naturally lead to higher savings without adjusting habits.

These patterns are normal. The key is noticing them early.

Worried About Lifestyle Creep?

If you want help understanding how lifestyle creep shows up in your own finances, our advisors can walk you through the details. Schedule a consultation to continue the conversation.

How to Avoid Lifestyle Creep

Pre-commit income increases

One practical approach to avoid lifestyle creep is to decide in advance how much of any income increase will go to spending and how much will go to saving. Even a modest commitment can protect long-term goals while still allowing room for improved quality of life. This can be especially useful for people receiving equity compensation, where income may come in irregular cycles.

Review fixed expenses annually

It also helps to revisit fixed expenses once a year and assess whether they still align with what you value. Not every subscription or upgrade needs to be cut. The goal is awareness. Clear visibility into where money goes makes it easier to make grounded decisions rather than reactive ones.

Adjust as life changes

Finally, remember that financial situations differ. Some years may call for more saving, and others may require more spending flexibility. A steady review process can help you adapt without losing progress toward longer-term plans.

Life Transitions That Trigger Lifestyle Creep

Lifestyle creep tends to appear during periods of rising income or changing roles.

It is especially common when:

Tech employees are experiencing rapid increases in salary or equity vesting

Individuals are transitioning from early-career pay to mid-level or senior compensation

Founders or startup employees are preparing for a liquidity event

Households are moving to higher cost-of-living areas

Someone who has an income that fluctuates meaningfully year to year

These transitions can be positive, but they also create opportunities for spending to grow faster than intended.

Wrapping Up

Lifestyle creep is not about avoiding comfort. It is about making sure your spending decisions support both your current needs and your future goals. When you understand how expenses grow and how taxes affect each raise, it becomes easier to keep savings on track and maintain financial flexibility.

Every financial situation is unique, but building healthy margins early often creates lasting benefits.

DISCLOSURES

DiversiFi Capital LLC is a registered investment adviser located in CA and may only transact business or render personalized investment advice in those states and international jurisdictions where we are registered, notice filed, or where we qualify for an exemption or exclusion from registration requirements. Any communications with prospective clients residing in jurisdictions where DiversiFi Capital LLC is not registered or licensed shall be limited so as not to trigger registration or licensing requirements.

Past performance is not indicative of future returns, and investing always carries inherent risks, including the potential loss of principal capital. Any investment strategies are specific to individual clients and may not be representative of the experiences of all clients.

The Information presented in our blog posts is intended for educational purposes only. It is not intended to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Unless otherwise stated, the investments discussed in our blog posts are not guaranteed.

The content in our blog posts is designed to provide information and insights but should not be used as the sole basis for making financial decisions. The content provided in our blog post(s) is provided “as is,” and/or “as available.” Diversifi Capital LLC will to the best of its abilities maintain the content to be up to date. However, Diversifi Capital LLC does not represent or warrant that our content or our services found within are accurate, complete, reliable, current, or error-free.

We strongly encourage readers to conduct their own research, seek advice from qualified financial professionals, and consider their unique financial circumstances before making any investment or financial decisions. Your individual situation may vary, and it's essential to make informed choices that align with your specific goals and needs.