Turning Equity Compensation into a Home: Sara & Jeff’s Home-Buying Journey

Disclosure:

This testimonial was given by a current client of DiversiFi Capital LLC, and it is not representative of all client experiences. No cash or compensation was given for or to elicit this testimonial.

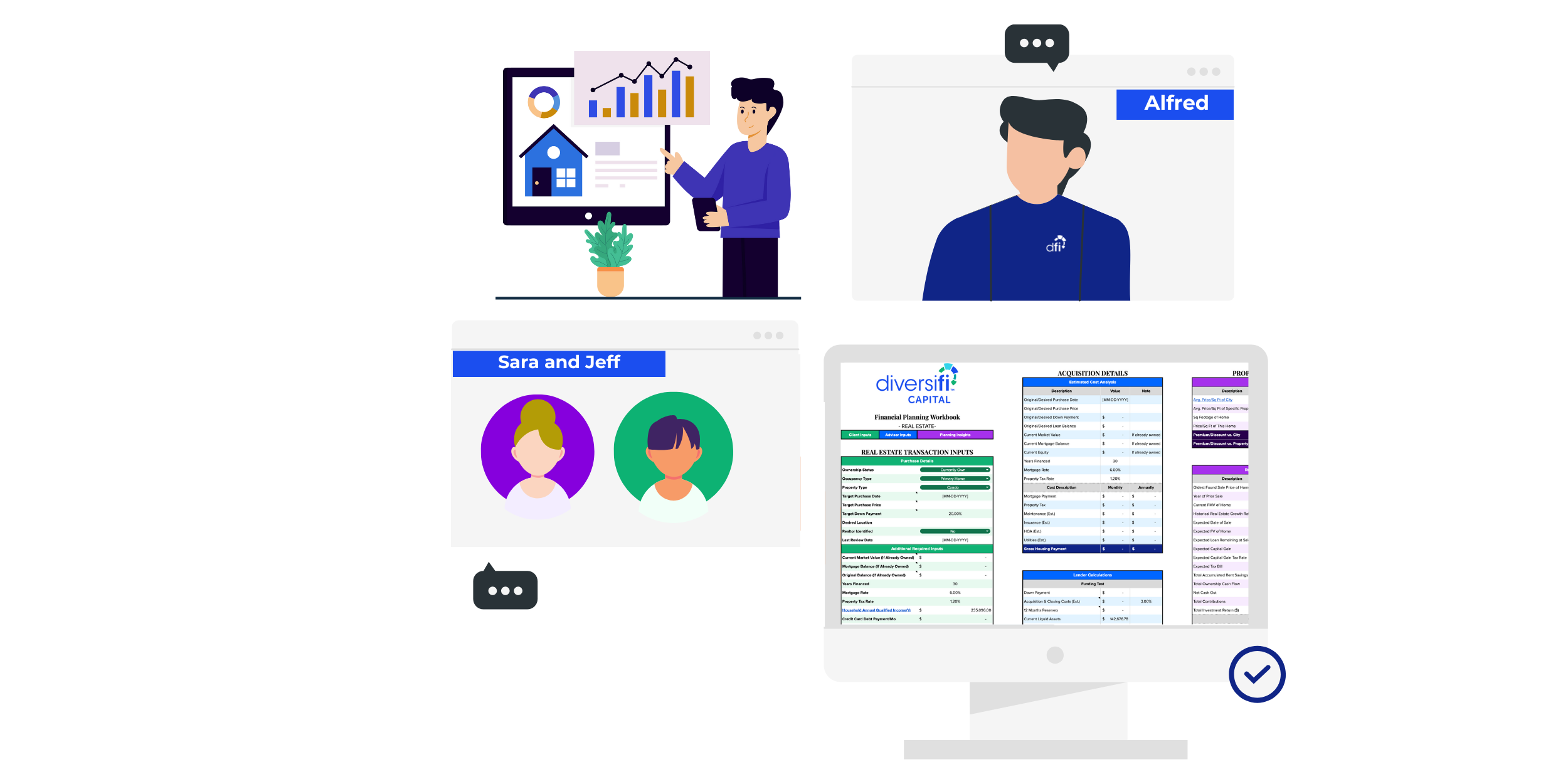

Meet Sara and Jeff, a powerhouse couple navigating the tech world and big life changes. Sara, now VP of Community at Chime (formerly at Lyft), and Jeff, a Sr. Campaigns Manager at Lyft, both made the leap into tech from the private sector. With that jump came a big shift: a major increase in income and, along with it, a whole new world of equity compensation that felt like a mystery. RSUs? Selling shares? It all felt theoretical rather than real tangible money until Alfred stepped in.

Like many growing families, Sara and Jeff dreamed of upgrading their living situation, but the uncertainty of how much home they could actually afford kept them hesitant. With a mix of strategic planning, clear education, and ongoing support, Alfred helped them turn their financial ambiguity into confidence. He worked with them to regularly sell vested shares, reinvest strategically, and create a sustainable financial plan that kept their future secure. He also provided education on budgeting, mortgage planning, and long-term wealth strategy. The result? In 2020, Sara and Jeff confidently bought a home at the higher end of their budget, taking advantage of historically low interest rates. What once felt like a leap of faith became a calculated, empowering move. Now, their home isn’t just a place to live; it’s a cornerstone of their long-term financial success and family life.

Sara and Jeff’s story is proof that with the right guidance, what feels overwhelming can become an exciting, well-planned milestone. In this interview, they share more about how working with Alfred gave them the confidence to take the next big step.

The Challenge

Before working with Alfred, what were your biggest concerns or uncertainties about buying a home? What were your initial thoughts/feelings about your equity compensation, and how did that influence your hesitation in moving forward with a home purchase?

Before working with Alfred, Sara and Jeff were hesitant to buy a home because they were financially cautious by nature, unsure how to navigate equity compensation, and afraid to overextend themselves in a high-cost market. Despite increased earnings in tech, they felt wary of treating stock as real income, and they didn’t feel confident making such a big decision without clear data and a plan aligned with their values.

“Despite being risk-takers in other capacities, we are both pretty conservative when it comes to financial risk. We really value a balance of agency and security, which were two things we bonded over when we were first dating. We want to be able to travel together, have our time be our own, and say no to jobs that don’t align with our values and personal growth goals.

Over the course of ten years each in the public sector, we worked really hard to avoid credit card debt, keep our spending in check, build an emergency savings fund, and invest in our retirements, despite salaries that were often pretty modest. We saved for a down payment on our first home aggressively during this era, but home ownership was always just out of reach, especially living in high-cost-of-living cities. We looked into other ways to afford owning our first home: rent arbitrage, moving to lower COLA cities, Airbnb, you name it, we considered it!

When we both joined the tech world around the same time, our salaries increased in foreign ways (stock compensation?!?), but our financial mental models stayed the same.

We were nervous to spend the portion of our compensation that was now paid in equity since it wasn’t “for sure,” and we had seen far too many people live on the salaries they wished they had, instead of the salaries they actually had. We wanted to be responsible and financially healthy, but we didn't know what that required in this new context.

Alfred helped us slowly get comfortable with a different way of financial planning, first identifying our risk tolerance and core values and then incorporating the same risk tolerance and values that we had before into a new set of circumstances.

Over the course of a few quarters, we built a full-life financial model, accounting for current and potential future costs (like a second kid, or a second car…or a first home!). Most notably, Alfred showed us comparative data on people in our financial bracket that contextualized the types of spending, saving, investing, and mortgage we could now afford in low-risk, medium-risk, or high-risk scenarios.

We ended up using these new models to make an offer on our first home: a fixer-upper in the nicest neighborhood we could have ever imagined. The price was still less than the mortgage company told us we could afford (which made us feel safe!!), but definitely a lot more than we would have ever felt comfortable spending without Alfred’s counsel.

Because of the confidence Alfred instilled in us and the data he provided us, we were also able to optimize the timing of our offer, moving when the hot housing market was temporarily stalled right after the 2020 election. We landed the first offer we made!

Sure, we could have rent-arbitraged or moved to a lower COLA out-of-state city— but Alfred helped us realize that those choices wouldn't have met our family’s growing, long-term needs in the same strategic ways.

At a 2.75% fixed interest rate, and with the home improvements we’ve made, our house has ended up being one of our best financial, community, family, and life decisions ever. Most people can’t say this: but because of smart research and introspection that Alfred helped us do, our first home is also our last & forever family home.”

Alfred’s Approach

How did Alfred guide you through the home purchase process to help you achieve your goal of buying a home? What approaches (strategic, tactical, and emotional) did he take to make you feel comfortable enough to make the leap? What’s one thing Alfred did that stood out as valuable to you?

Alfred helped them reframe financial decisions as value-driven opportunities, guiding them through scenario-based planning to balance ambition with stability. The result was a confident home purchase that supports both their long-term goals and day-to-day happiness.

“Alfred helped remind us that money is a tool and that it can actually be financially healthy to take “big swings” with our tools — when we’re leveraging it for things we really, really value, in responsible ways. He also helped us understand that a “big swing” is relative.

We are both huge homebodies, design nerds, and community builders, and our house and neighborhood have brought us pretty endless joy. Five years in, we still actually enjoy weekend chores and fix-it tasks. We consider our neighbors some of our closest family friends. Homeownership really suits us in ways that some of the other options we looked into would not have.

Secondly, our fixed-rate mortgage has stayed the same while careers have grown and our compensation has increased. We didn’t buy the safest, least expensive home that our instincts told us to go for, and thank goodness because we don't have to be back on the housing market in two years (or even ten years!). We also didn’t buy a home that was so ambitious that we had to stop traveling together, feeling safe in our financial health, or doing other things we love.

Alfred wove all of these hopes and fears into concrete, simple financial models. He showed us what would happen if one of us lost a job, if both of us did, and the opposite: what would happen if we made more?!

Data-rooted scenario planning is something we did a ton of at work but not a ton of in our personal lives. Alfred translated this orientation beautifully.”

The Outcome

What outcomes did you achieve through Alfred’s support, strategies, and guidance? What were the highlights? What was the impact of these outcomes? Thinking back, how did your feelings about buying a home change before working with Alfred versus after? What changed for you?

Alfred gave them the confidence to make values-based financial decisions and navigate a changing financial landscape. Since buying their home, his ongoing support has helped them manage their other life changes smoothly and empowered them to confidently make important values-aligned financial decisions.

“Alfred gave us the confidence and context to make values-aligned decisions in a new financial landscape.

Since buying our home, he’s continued to support us through job changes, two kids, childcare budgeting, retirement planning, and diversification. He’s helped us avoid money fights, make smarter choices, and stay aligned as a couple.

Honestly, working with him has been one of the best investments we’ve made in our marriage!”

Recommend?

Would you recommend Alfred and DiversiFi to other Chime and Lyft employees or those in similar situations who are interested in buying a home or making a big purchase in general? If so, why? What’s one thing you would want them to know about working with Alfred or DiversiFi?

“Definitely. Spend the time and commit to getting a full financial plan, and then stick to the quarterly meetings. You’ll learn a ton about yourself and your partner and build new shared values, practices, and mental models along the way that help you reach for new horizons.”

DiversiFi’s Final Thoughts

Navigating equity compensation and home buying simultaneously can feel like learning a new language while making one of the biggest decisions of your life. For Sara and Jeff, the jump into tech brought more income and opportunity but also more complexity and uncertainty. They didn’t just want to buy a house; they wanted to make a move that aligned with their values, lifestyle, and future goals. That’s where Alfred came in. With deep experience helping clients turn theoretical equity compensation into tangible, strategic outcomes, Alfred empowered them to view their equity compensation as a tool they could use to achieve real-life goals. He helped them model different financial scenarios, evaluate trade-offs, and build a plan rooted in what mattered most to them. His approach wasn’t just about closing on a home. It was about unlocking long-term confidence. Today, that home isn’t just their residence. It’s the physical expression of the life they worked hard to build and the peace of mind that comes with knowing it was a decision backed by both heart and strategy.

Ready to get started on your financial wellness journey?

DiversiFi Capital LLC is a registered investment adviser located in CA and may only transact business or render personalized investment advice in those states and international jurisdictions where we are registered, notice filed, or where we qualify for an exemption or exclusion from registration requirements. Any communications with prospective clients residing in jurisdictions where DiversiFi Capital LLC is not registered or licensed shall be limited so as not to trigger registration or licensing requirements.

Past performance is not indicative of future returns, and investing always carries inherent risks, including the potential loss of principal capital. Any investment strategies are specific to individual clients and may not be representative of the experiences of all clients.

Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed.